You do not need to be a UAE resident to buy property in Dubai. In fact, thousands of overseas investors purchase Dubai real estate every year from countries like the UK, India, China, Russia, and across Europe and Africa — many of them specifically to qualify for the Golden Visa.

But buying property remotely comes with unique challenges: different mortgage rules, international money transfers, power of attorney requirements, and a process that can feel overwhelming when you are not on the ground. This guide covers every step of buying Dubai property as a non-resident, from initial research to Golden Visa approval.

Disclaimer: Property laws, mortgage requirements, and visa processes may change. This guide reflects conditions as of early 2026. Always verify current requirements with official sources, RERA-certified agents, and licensed mortgage advisors.

Table of Contents

- Can Non-Residents Buy Property in Dubai?

- Resident vs Non-Resident: Key Differences

- Step-by-Step Purchase Process

- Non-Resident Mortgage Options

- Transferring Money to Dubai

- Power of Attorney Guide

- Complete Cost Breakdown

- Case Study: UK Buyer’s Journey

- Essential Tips for Overseas Buyers

- Frequently Asked Questions

- Conclusion

Can Non-Residents Buy Property in Dubai?

Yes, absolutely. Since 2002, foreign nationals of any nationality can purchase property in Dubai’s designated freehold areas. There are no restrictions based on nationality, no residency requirement for purchase, and you receive full freehold ownership rights — the same as a UAE national.

Key facts for non-resident buyers:

- No residency required: You can buy from anywhere in the world

- Full ownership rights: Freehold ownership, inheritable, no time limits

- No nationality restrictions: Open to all nationalities

- No annual property tax: Only a one-time 4% DLD transfer fee

- Golden Visa eligible: Properties AED 2M+ qualify you for a 10-year visa

- Rental income: Tax-free rental income even as a non-resident landlord

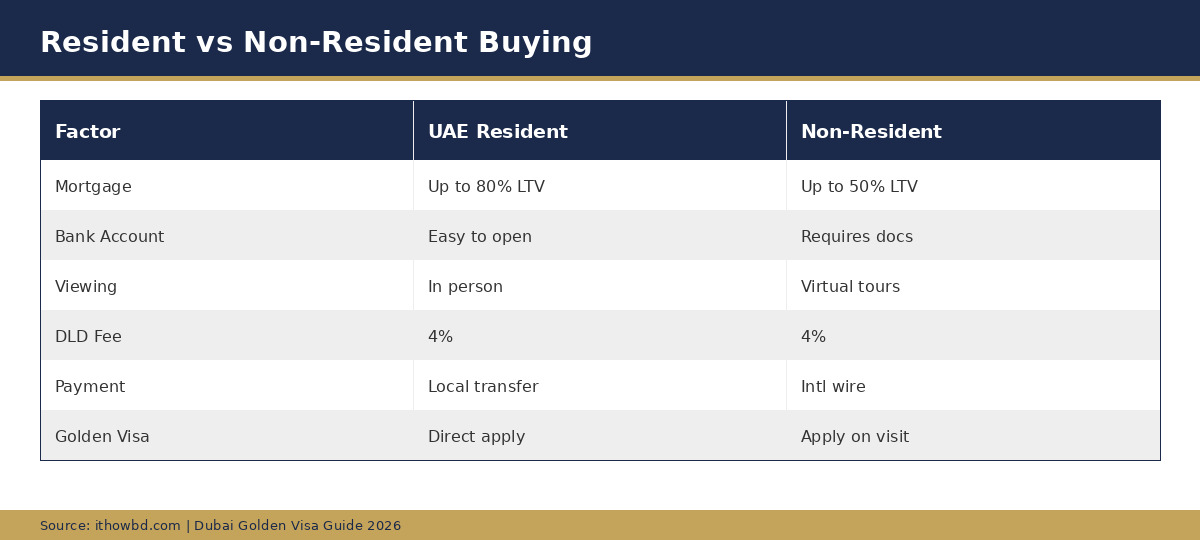

Resident vs Non-Resident: Key Differences

While non-residents have full rights to buy, there are practical differences in the buying process:

Mortgage Access

This is the biggest difference. UAE residents can access up to 80% LTV (Loan-to-Value) mortgages for their first property. Non-residents are typically limited to 50% LTV, meaning you need to bring at least 50% of the property value as a down payment. For a AED 2M property, that is AED 1,000,000 minimum cash required.

For a detailed analysis of mortgage options, see our mortgage guide.

Bank Account Requirements

You will need a UAE bank account to complete the purchase and receive rental income. Some banks allow non-residents to open accounts remotely, while others require an in-person visit. Plan this early in your buying process.

Physical Presence

While you can do much of the research and initial steps remotely, most transactions require at least one visit to Dubai — for property viewing, DLD registration, and bank account setup. Alternatively, a Power of Attorney can handle many steps on your behalf.

Power of attorney documents must be attested by the UAE Ministry of Economy or relevant notary.

Step-by-Step Non-Resident Purchase Process

Phase 1: Remote Research (2–4 weeks)

- Define your budget and goals: Investment property, personal use, or both? This determines the ideal area and property type

- Research areas: Use our freehold areas guide to shortlist 2–3 neighbourhoods

- Find a RERA-certified agent: Verify their registration number on the DLD website. A good agent will arrange virtual tours, provide market comparisons, and guide the entire process

- Get mortgage pre-approval: If financing, contact UAE banks that offer non-resident mortgages. Pre-approval gives you a clear budget and strengthens your negotiating position

- Start bank account process: Contact banks like Emirates NBD, ADCB, or HSBC (with international presence) about opening a UAE account

Phase 2: Property Selection (1–2 weeks)

- Virtual property tours: Most agents offer video walkthroughs, 3D tours, and live video calls from the property

- Visit Dubai (recommended): While not always required, we strongly recommend at least one visit to see properties, experience neighbourhoods, and meet your agent in person

- View 5–10 properties: Compare across your shortlisted areas. For off-plan, visit showrooms and model apartments. See our off-plan vs ready comparison to decide your strategy

- Negotiate and make an offer: In Dubai, negotiation of 5–10% below asking is normal for resale properties. Off-plan prices from developers are generally fixed

Phase 3: Purchase and Registration (1–2 weeks)

- Sign MOU (Form F): Memorandum of Understanding outlining terms, price, and timeline. Pay a 10% deposit (held in escrow)

- Obtain NOC from developer: Required for resale properties. Developer confirms no outstanding charges

- Transfer payment: Wire remaining funds to the escrow/trust account or directly as instructed

- DLD registration: Both buyer and seller (or authorized representatives via POA) attend the Dubai Land Department (DLD). Pay the 4% transfer fee. Title Deed issued same day

- For off-plan: Sign SPA (Sale and Purchase Agreement) with the developer. Oqood registration happens through the developer at RERA

Phase 4: Golden Visa Application (2–4 weeks)

- Gather documents: Use our complete document checklist

- Apply through ICP or GDRFA Dubai: Can be done during a visit to Dubai or through an authorized service centre

- Medical test and biometrics: Must be completed in person in the UAE

- Visa approved: Typically 2–4 weeks after complete submission

- Sponsor family: Apply for spouse and children immediately after your visa is approved. See our family benefits guide

Non-Resident Mortgage Options

Several UAE banks offer mortgages to non-residents, though with stricter terms than resident mortgages:

Key Non-Resident Mortgage Terms

- Maximum LTV: 50% (you need 50% down payment minimum)

- Maximum tenure: 15–25 years

- Interest rates: 4.0–5.5% (slightly higher than resident rates)

- Minimum income: Varies by bank (typically AED 15,000–25,000 equivalent monthly income)

- Documentation: Salary certificates, bank statements (6–12 months), tax returns (for some countries)

Banks Offering Non-Resident Mortgages

- Emirates NBD: Up to 50% LTV, competitive rates, largest mortgage provider

- ADCB: Up to 50% LTV, good for Indian and UK nationals

- Mashreq Bank: Up to 45% LTV, flexible documentation requirements

- First Abu Dhabi Bank (FAB): Up to 50% LTV, strong for GCC nationals

- HSBC UAE: Up to 50% LTV, excellent for existing HSBC customers globally — can leverage international banking relationship

Pro tip: Start your mortgage application 4–6 weeks before your planned purchase. Non-resident applications take longer to process due to international document verification. See our dedicated mortgage options guide for detailed rate comparisons.

Transferring Money to Dubai

Moving large sums internationally requires planning:

International Wire Transfer

- Bank-to-bank SWIFT transfer: Most common method. Fees of 0.1–0.5% plus currency conversion

- Processing time: 1–5 business days depending on banks and countries involved

- Currency: Transfers can be in AED, USD, GBP, EUR, or other major currencies. AED is pegged to USD, so USD transfers are straightforward

- Documentation: Your bank may require proof of purpose (property purchase contract, MOU)

Forex Specialists

- Companies like Wise (TransferWise), OFX, or WorldRemit often offer better exchange rates than traditional banks

- Savings: Can save 1–3% on currency conversion compared to bank rates

- On a AED 2M transfer: This could mean AED 20,000–60,000 in savings

- Verify limits: Some services have maximum transfer limits that may require multiple transactions

Important Compliance Notes

- Keep all transfer receipts and documentation — you will need proof of source of funds

- Declare large transfers as required by your home country’s regulations

- Some countries have capital controls or reporting requirements for large international transfers

- The UAE has strict anti-money laundering regulations — be prepared to document the source of your funds

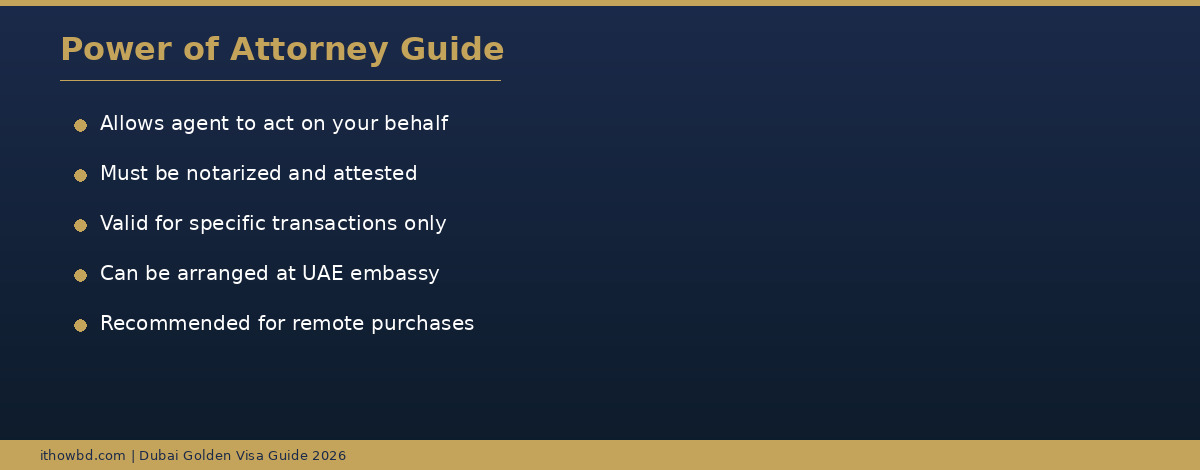

Power of Attorney: Buying Without Being Present

If you cannot be in Dubai for every step, a Power of Attorney (POA) allows a trusted person — typically your agent or lawyer — to act on your behalf for specific transactions.

How POA Works for Dubai Property

- Specific POA: Authorizes your representative to complete a specific property transaction. This is safer and more commonly used than general POA

- Where to get: At a UAE Embassy or Consulate in your country, or at a Notary Public (requires attestation)

- Cost: AED 500–2,000 depending on the embassy and attestation requirements

- Validity: Typically valid for the duration of the specific transaction (3–6 months)

- What it covers: Signing the MOU, completing DLD transfer, bank transactions related to the purchase

POA Best Practices

- Only grant specific POA for defined transactions — never general POA for all financial matters

- Use a reputable law firm (like Al Tamimi, Baker McKenzie, or Hadef & Partners)

- Include clear transaction limits and expiry dates in the POA document

- Keep copies of all POA documents and revoke immediately after transaction completion

Complete Cost Breakdown for Non-Residents

Beyond the property price, budget for these additional costs (approximately 7–8% of property value):

Mandatory Costs

- DLD transfer fee: 4% of property value — AED 80,000 on a AED 2M property

- DLD admin fee: AED 4,000–5,000

- Title Deed issuance: AED 250

- Agent commission: 2% of property value — AED 40,000 on a AED 2M property (usually paid by buyer)

If Using a Mortgage

- Mortgage registration fee: 0.25% of loan amount

- Bank arrangement fee: ~1% of loan amount

- Property valuation: AED 2,500–5,000

- Life insurance (bank requirement): ~0.4% of outstanding loan per year

Other Costs

- Developer NOC: AED 500–5,000

- Power of Attorney (if used): AED 500–2,000

- Legal fees (optional but recommended): AED 5,000–15,000

- Travel costs: Flights and accommodation for viewing trip(s)

Total Additional Costs Example (AED 2M Property)

- Cash purchase: ~AED 130,000–150,000 (6.5–7.5% of property value)

- With mortgage: ~AED 165,000–190,000 (8–9.5% of property value)

- Grand total with AED 2M property: AED 2,130,000–2,190,000

For a full ROI analysis including all costs, see our ROI calculation guide.

Case Study: UK Buyer’s Golden Visa Journey

This is an illustrative composite based on common buyer experiences.

Background: David, 42, is a London-based senior finance professional. He wanted to diversify his investments outside the UK, secure a tax-efficient base, and have a family holiday home in a warm climate.

Budget: AED 2,500,000 (approximately GBP 520,000 at the time of purchase).

The Process

- Month 1: Researched areas online, contacted 3 RERA-certified agents via email, received virtual tour packages for Downtown Dubai, Dubai Marina, and Business Bay

- Month 2: 5-day viewing trip to Dubai. Visited 12 properties. Applied for mortgage pre-approval with HSBC UAE (leveraging his UK HSBC account). Opened a UAE bank account with Emirates NBD

- Month 2 (end): Selected a 2BR apartment in Downtown Dubai for AED 2.5M. Signed MOU, paid 10% deposit (AED 250,000)

- Month 3: Mortgage approved at 50% LTV (AED 1.25M loan). Transferred remaining AED 1.25M from UK via HSBC international transfer. Completed DLD registration via his agent (POA arranged during visit)

- Month 3 (end): Title Deed received. Applied for Golden Visa during a second 3-day trip. Completed medical test and biometrics

- Month 4: Golden Visa approved. Applied for spouse and 2 children. All family visas approved within 3 weeks

Total timeline: 4 months from first research to family visa approval. Total investment (including all fees): approximately AED 2.69M. The property is now managed by a professional property management company for short-term holiday rentals when the family is not using it.

For more real investor stories, see our expat success stories collection.

Essential Tips for Overseas Buyers

- Only use RERA-registered agents. Verify their registration on the DLD website or Dubai REST app. Unregistered agents are illegal and offer no consumer protection

- Verify freehold status. Confirm the property is in a designated freehold area before committing. Our freehold areas guide has the complete list

- Open a UAE bank account early. This can take 2–4 weeks for non-residents and is required for property registration and receiving rental income

- Budget 7–8% for additional costs. Do not spend your entire budget on the property price — you need reserves for DLD fees, agent commission, and other costs

- Use escrow for off-plan purchases. RERA requires developers to use escrow accounts, protecting your payments during construction

- Get independent legal advice. Especially for your first Dubai purchase, a property lawyer (AED 5,000–15,000) can save you from costly mistakes

- Consider property management. If you will not be in Dubai, a professional manager (8–15% of rental income) handles tenant sourcing, maintenance, and rent collection

Frequently Asked Questions

Can I buy Dubai property entirely from abroad without visiting?

Technically yes, using a Power of Attorney. Your appointed representative can sign documents, complete DLD registration, and handle the entire transaction. However, for the Golden Visa application, you need to be in the UAE for the medical test and biometrics. Most experts recommend at least one viewing trip before committing to a multi-million dirham purchase — photographs and virtual tours cannot fully replace being there in person.

Do non-residents pay higher DLD fees or property taxes?

No. Non-residents pay the exact same DLD transfer fee (4%) and have the same zero annual property tax as UAE residents. There is no discrimination in fees or taxes based on residency status. The only practical difference is in mortgage terms — non-residents can typically borrow up to 50% LTV compared to 80% for existing residents.

Which banks offer the best non-resident mortgages?

Emirates NBD, ADCB, First Abu Dhabi Bank (FAB), and HSBC UAE are the most active in non-resident mortgages. HSBC is particularly strong for buyers who already have an HSBC account in their home country. All offer up to 50% LTV. Rates range from 4.0% to 5.5% depending on the bank, property type, and your financial profile. Apply to at least 2–3 banks to compare offers.

How do I safely transfer large amounts of money to Dubai?

Use bank-to-bank SWIFT transfers or reputable forex specialists like Wise or OFX. Always transfer to your own UAE bank account or a regulated escrow account — never to an agent’s personal account. Keep all transfer receipts and source-of-funds documentation. Budget for 0.1–0.5% in transfer fees plus currency conversion costs. For large transfers, forex specialists can save 1–3% compared to bank exchange rates.

What happens to my property if I do not get the Golden Visa?

Your property ownership is completely independent of your visa status. Even if you do not apply for or do not receive a Golden Visa, you still own the property with full freehold rights. You can rent it out, sell it, visit it on tourist visas, or pass it to heirs. The Golden Visa is an additional benefit of owning property valued at AED 2M+ — it is not a requirement of property ownership.

About the Author

Editorial Team — ithowbd.com

Our team specializes in supporting international buyers through the Dubai property acquisition process. We work with overseas investors from 30+ countries and understand the unique challenges of cross-border property purchases.

Conclusion: Distance Is No Barrier

Buying Dubai property as a non-resident is straightforward when you approach it systematically. The process is well-established, the legal framework protects buyers, and the Golden Visa provides a powerful incentive to invest.

The key is preparation: find a trusted RERA agent, open your bank account early, get mortgage pre-approval, and plan at least one viewing trip. With the right preparation, you can go from initial research to Golden Visa holder in 3–4 months.

Explore our full guide series: Top Freehold Areas, Best Developers, Mortgage Options, and Document Checklist.

Last updated: February 2026.