Are you an expat in Dubai thinking about investing in property to qualify for the UAE Golden Visa? You are not alone. Thousands of foreign nationals are exploring real estate as a pathway to long-term residency in the UAE. But here is the big question that stops most investors: should you buy off-plan or ready property for your Golden Visa?

This decision can mean the difference between a 28% capital gain and a stagnant investment. It affects your visa timeline, rental income, risk exposure, and even your family benefits of UAE Golden Visa‘s future in the UAE. In this comprehensive guide, we break down everything you need to know about off-plan vs ready properties for Golden Visa in Dubai — with real payment plans, ROI projections, and honest risk assessments based on 2025–2026 market data.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Property investment carries risks. Always consult a licensed real estate advisor and legal professional before making investment decisions. Data referenced is from public sources and may have changed since publication.

Table of Contents

- What Are Off-Plan and Ready Properties?

- Golden Visa Eligibility: Property Requirements

- Step-by-Step Buying Process

- Payment Plan Structures Compared

- ROI Projections: Off-Plan vs Ready

- Risk Assessment and Mitigation

- Dubai Property Market Data 2024–2026

- Head-to-Head Comparison Table

- Case Study: Ahmed’s Golden Visa Journey

- Frequently Asked Questions

- Conclusion and Final Verdict

What Are Off-Plan and Ready Properties in Dubai?

Off-Plan Properties Explained

An off-plan property is a unit you purchase directly from a developer before construction is complete — sometimes even before it starts. You are essentially buying based on architectural plans, 3D renders, and the developer’s reputation.

In Dubai, off-plan sales are regulated by the Real Estate Regulatory Authority (Real Estate Regulatory Authority (RERA)) under the Dubai Land Department (DLD). Developers must register projects, open escrow accounts, and meet construction milestones before collecting payments. This provides a layer of protection for buyers.

Key characteristics of off-plan properties:

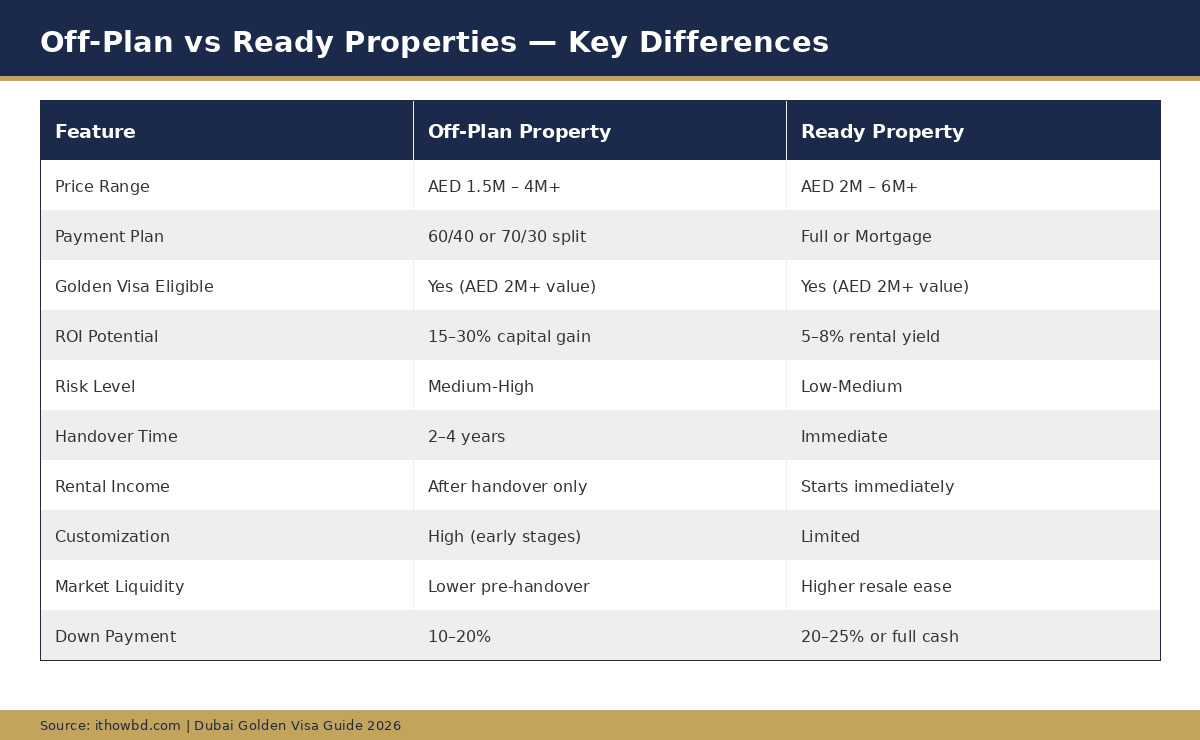

- Lower entry price — typically 10–30% below market value at launch

- Flexible payment plans — spread over construction period (2–4 years)

- Capital appreciation potential — value increases as construction progresses

- Customization options — choose floor, view, layout in early stages

- No immediate rental income — you must wait until handover

Ready Properties Explained

A ready property (also called “secondary market” or “completed property”) is a unit that is fully constructed, handed over, and available for immediate occupancy. You can physically inspect it, move in, or start renting it out right away.

Key characteristics of ready properties:

- What you see is what you get — physical inspection before purchase

- Immediate rental income — start earning from Day 1

- Instant Golden Visa eligibility — apply immediately after purchase

- Established communities — amenities, transport, schools already operational

- Higher upfront cost — market-rate pricing, less negotiation room

Golden Visa Eligibility: Property Investment Requirements in 2026

The UAE Golden Visa through property investment requires a minimum real estate value of AED 2,000,000 (approximately USD 545,000). This threshold was updated in October 2022 when the UAE government reformed the Golden Visa program.

Key Eligibility Rules

- Property must be in a freehold designated area (e.g., Downtown Dubai, Palm Jumeirah, Dubai Marina, JVC, Business Bay)

- Minimum value of AED 2 million based on the purchase price or DLD valuation

- Property can be fully paid or mortgaged — but the total value must meet the threshold

- Off-plan properties qualify if the total contract value is AED 2M+, even if not fully paid yet

- You can combine multiple properties to reach the AED 2M threshold

- The Golden Visa is valid for 10 years and is Golden Visa renewal rules

- You can sponsor your spouse, children, and parents under the same visa

Off-Plan vs Ready: Golden Visa Timing Difference

This is a critical distinction that many investors miss:

- Ready property: You can apply for Golden Visa immediately after completing the purchase and receiving your Title Deed

- Off-plan property: You can apply for Golden Visa once the property is registered with DLD and you receive your Oqood (initial registration certificate) — even during construction. However, some cases require the Title Deed at handover

Since 2023, Dubai has allowed Golden Visa applications with Oqood certificates for off-plan properties valued at AED 2M+, which was a major policy change benefiting off-plan investors. However, requirements may vary based on individual circumstances. Always confirm current rules with ICP (Federal Authority for Identity and Citizenship) or GDRFA.

Step-by-Step Process: Buying Property for Golden Visa

Buying Off-Plan Property: The Process

Here is the typical journey when purchasing an off-plan property in Dubai for Golden Visa purposes:

- Research RERA-approved developers — Check the Dubai Land Department portal for registered projects. Focus on Tier-1 developers like Emaar, DAMAC, Sobha, Nakheel, and Meraas

- Select a project valued at AED 2M+ — Ensure the unit price meets the Golden Visa threshold. Consider location, payment plan, and expected completion date

- Pay the booking fee — Typically 1–5% of the property value to reserve your unit

- Sign the Sales Purchase Agreement (SPA) — Review all terms, payment schedule, handover date, penalty clauses, and cancellation policy with a lawyer

- Pay DLD registration fees — 4% of property value + AED 580 admin fee + AED 5,250 Oqood registration

- Follow the payment schedule — Construction-linked installments as per SPA (e.g., 10% at slab, 10% at structure, etc.)

- Receive Oqood certificate — This is your initial ownership registration. You may apply for Golden Visa at this stage

- Handover and Title Deed — Upon project completion, receive keys and final Title Deed

- Apply for Golden Visa — Submit documents through ICP or GDRFA portal

Buying Ready Property: The Process

- Search properties — Use platforms like Property Finder, Bayut, or work with a RERA-certified agent

- Inspect the property physically — Check condition, view, amenities, and neighborhood

- Make an offer and negotiate — Ready properties have more room for price negotiation

- Arrange financing — If using a mortgage, get pre-approval from a UAE bank

- Sign MOU (Form F) — Memorandum of Understanding with 10% deposit

- Complete NOC and transfer — Seller obtains No Objection Certificate from developer. Transfer ownership at DLD

- Pay DLD fees — 4% transfer fee + admin charges + agent commission (typically 2%)

- Receive Title Deed — Immediate title deed issuance

- Apply for Golden Visa — Submit documents the same week

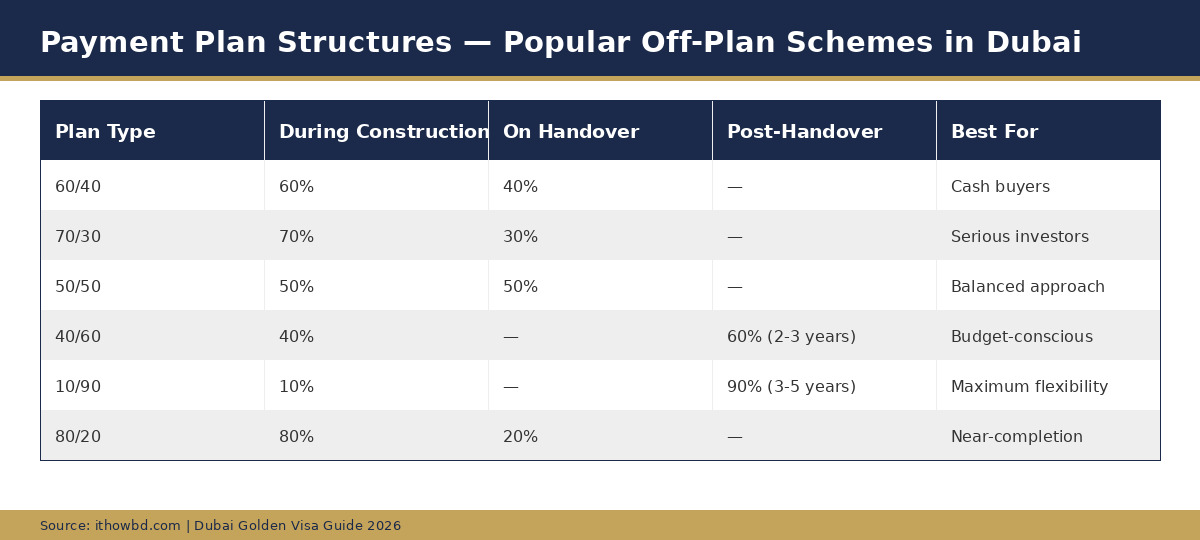

Payment Plans: How Developers Structure Off-Plan Payments

One of the biggest advantages of off-plan properties is the flexible payment plan. Unlike ready properties where you need full payment or a mortgage upfront, off-plan developers spread payments across the construction period — and sometimes even years after handover.

Most Common Off-Plan Payment Plans in Dubai

60/40 Plan: You pay 60% during construction and 40% on handover. This is the most traditional structure. Emaar frequently uses this for premium projects in Downtown and Dubai Hills.

80/20 Post-Handover: Pay 80% during construction with only 20% due after handover, spread over 1–2 years. DAMAC and Sobha often offer this structure.

10/90 or 20/80 Plans: Pay just 10–20% during construction and the remaining 80–90% post-handover over 3–5 years. This offers maximum cash flow flexibility but may come with slightly higher total prices.

Real Example: AED 2.2M Apartment in Dubai Hills

Let us say you purchase a 2-bedroom apartment in Dubai Hills Estate from Emaar for AED 2,200,000 with a 60/40 payment plan over 30 months of construction:

- Booking: AED 110,000 (5%)

- 1st installment (3 months): AED 220,000 (10%)

- 2nd installment (6 months): AED 220,000 (10%)

- 3rd installment (12 months): AED 220,000 (10%)

- 4th installment (18 months): AED 220,000 (10%)

- 5th installment (24 months): AED 330,000 (15%)

- On handover (30 months): AED 880,000 (40%)

Total paid during construction: AED 1,320,000. Remaining at handover: AED 880,000 (can arrange mortgage at this point).

Ready Property Payment Options

For ready properties, you typically have two options:

- Cash purchase: Full payment at transfer. Best for negotiating a lower price (5–10% discount possible)

- Mortgage: UAE banks offer up to 75% LTV for residents and 50% LTV for non-residents. Interest rates range from 3.99% to 5.5% (fixed for 1–5 years). Monthly payments on AED 2M with 25% down at 4.5% over 25 years ≈ AED 8,300/month

ROI Projections: Where Does Your Money Grow Faster?

This is where the off-plan vs ready debate gets really interesting. Both types offer different ROI profiles, and the “better” option depends on your investment goals, risk tolerance, and timeline.

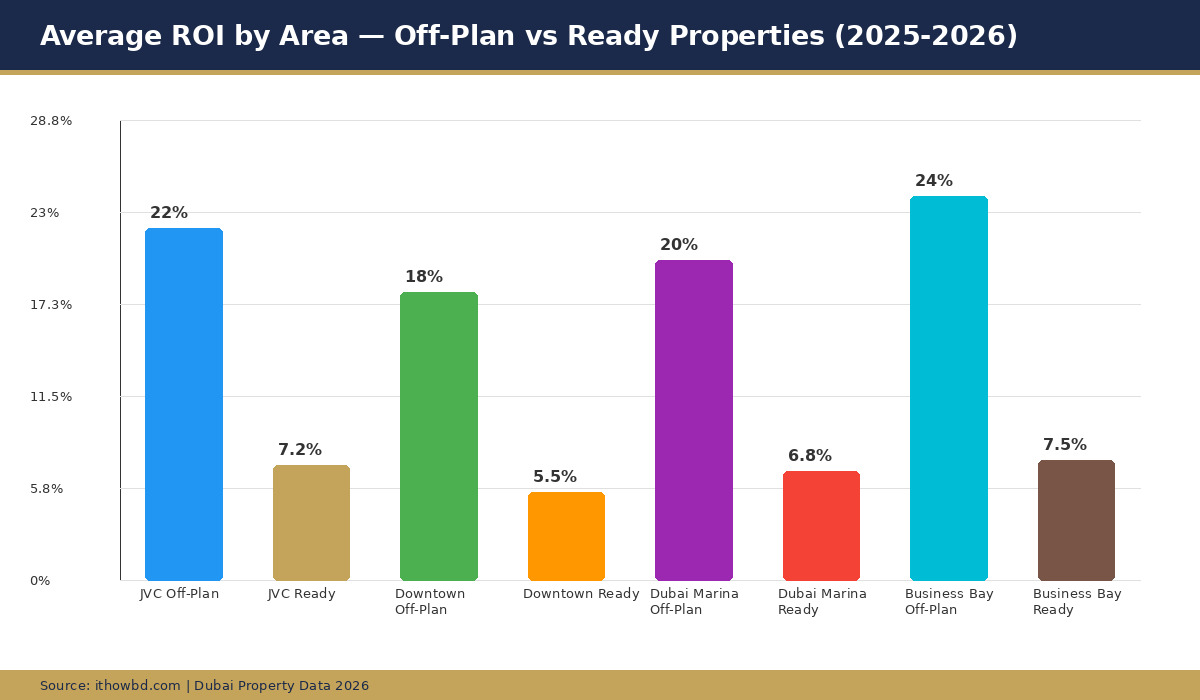

Off-Plan ROI: Capital Appreciation Focus

Off-plan properties primarily generate returns through capital appreciation — the increase in property value from launch price to market value at handover or resale. Based on 2023–2025 market data from the Dubai Land Department:

- Business Bay: 20–28% average appreciation from launch to handover

- Dubai Hills Estate: 18–25% appreciation over 2–3 year construction period

- JVC (Jumeirah Village Circle): 15–22% appreciation, strong value-for-money area

- Dubai Marina: 18–24% appreciation for waterfront units

- Downtown Dubai: 15–20% appreciation (already premium-priced at launch)

Important caveat: These are historical figures from a bull market period. Past performance does not guarantee future results. The Dubai property market has experienced cycles, including the 2008–2010 correction where some off-plan properties lost 40–60% of their value.

Ready Property ROI: Rental Yield Focus

Ready properties generate returns primarily through rental yields — the annual rental income as a percentage of property value. Dubai remains one of the highest-yielding property markets globally:

- JVC: 7.0–8.5% gross rental yield (highest in Dubai for apartments)

- Business Bay: 6.5–7.8% gross rental yield

- Dubai Marina: 6.0–7.2% gross rental yield

- Downtown Dubai: 5.0–6.0% gross rental yield

- Palm Jumeirah: 4.5–6.0% gross rental yield (higher for villas)

Net rental yields (after service charges, maintenance, and management fees) are typically 1.5–2% lower than gross figures.

5-Year ROI Comparison Example

Let us compare two scenarios for an AED 2.2M investment:

Scenario A: Off-Plan in Business Bay

- Purchase: AED 2,200,000 (60/40 plan, paid over 2.5 years)

- Capital appreciation by handover: ~24% = AED 528,000

- Rental income years 3–5 (after handover): AED 165,000/year × 2.5 years = AED 412,500

- Total 5-year return: AED 940,500 (42.7% total ROI)

Scenario B: Ready Property in JVC

- Purchase: AED 2,200,000 (cash or mortgage)

- Capital appreciation over 5 years: ~15% = AED 330,000

- Rental income years 1–5: AED 165,000/year × 5 = AED 825,000

- Total 5-year return: AED 1,155,000 (52.5% total ROI)

Note: These projections use moderate estimates. Actual returns vary based on market conditions, location, property type, and management quality. Numbers exclude transaction costs, service charges, and taxes.

Risk Assessment: What Could Go Wrong?

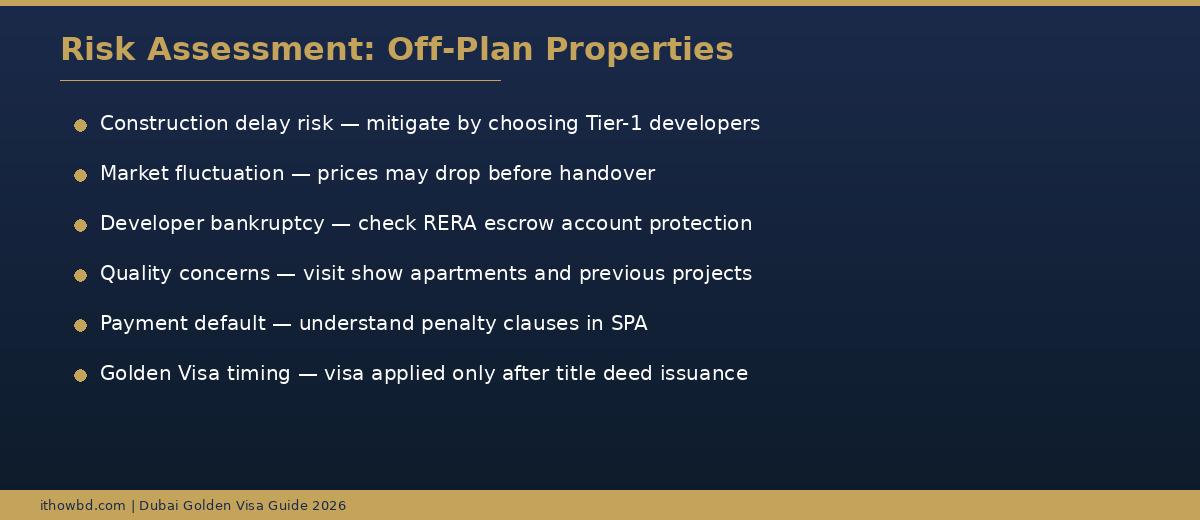

Off-Plan Property Risks

- Construction delays: Projects can be delayed by 6 months to 2+ years. This postpones your Golden Visa application, rental income, and potentially affects your residency status

- Developer bankruptcy: Although RERA’s escrow laws protect buyers, there have been cases where projects were cancelled. Research the developer’s track record thoroughly

- Market downturn: If property values drop during construction, your unit may be worth less than what you paid at handover

- Quality discrepancies: The delivered product may differ from showroom displays and marketing materials

- Payment default penalties: If you cannot keep up with installments, you may lose your deposit and face legal action

- Oversupply risk: Dubai’s construction pipeline is massive. An oversupply in a specific area can suppress prices and rents

Ready Property Risks

- Higher entry cost: You need more capital upfront, reducing diversification options

- Hidden defects: Older properties may have structural issues, outdated systems, or high maintenance costs

- Service charge increases: Annual fees can rise significantly, eating into rental yields

- Tenant issues: Non-payment, property damage, or extended vacancies affect your returns

- Market timing: Buying at peak prices means less capital appreciation potential

Risk Mitigation Strategies

- For off-plan: Choose Tier-1 developers (Emaar, Nakheel, Meraas, Sobha) with proven delivery records. Verify RERA registration number. Check escrow account details. Visit completed projects by the same developer

- For ready: Hire an independent property inspector (snagging expert). Review 3+ years of service charge history. Check occupancy rates in the building. Get a professional property valuation before purchase

- For both: Never invest money you cannot afford to lose. Diversify across areas if possible. Keep 6–12 months of mortgage payments as emergency reserve. Work with RERA-certified agents only

Dubai Property Market Data: 2024–2026 Trends

Understanding the broader market context is essential for making an informed investment decision. Here are key statistics from official sources:

Transaction Volume Trends

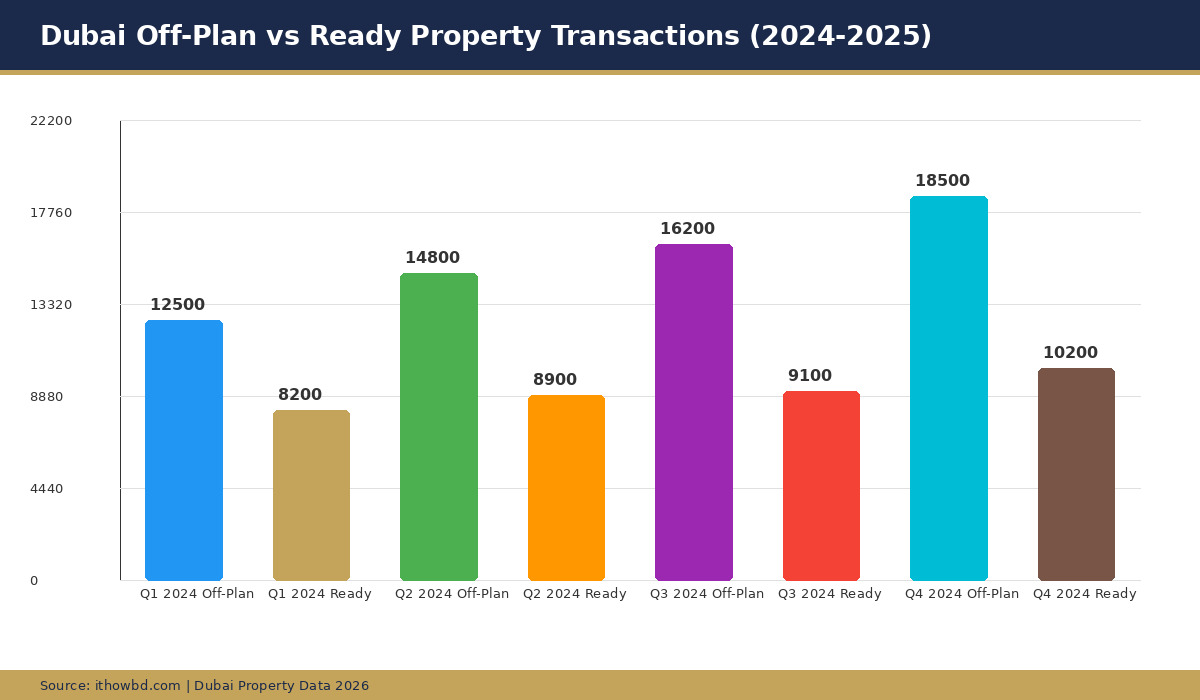

According to the Dubai Land Department, real estate transactions reached record levels in 2024:

- Total 2024 transactions exceeded 180,000+ property deals

- Off-plan transactions accounted for approximately 62% of total volume

- Ready/secondary market transactions made up the remaining 38%

- Total transaction value surpassed AED 522 billion in 2024

- Average apartment prices increased 12–18% year-over-year in prime areas

Golden Visa Applications Through Property

- Property-based Golden Visa applications increased by 45% in 2024 compared to 2023

- The average property value for Golden Visa applicants was AED 2.8 million

- Processing time averaged 15–30 business days from complete application submission

- Approval rate for property investors with complete documentation exceeded 95%

2026 Market Outlook

Industry analysts from major real estate consultancies (JLL, Knight Frank, CBRE) generally project moderate growth for Dubai’s property market in 2026, though opinions vary:

- Continued population growth (Dubai targets 5.8 million residents by 2040)

- Infrastructure expansion including Dubai Metro extensions and new developments

- Potential moderation in price growth after 3 years of strong appreciation

- Increasing supply from off-plan handovers may stabilize or soften prices in some areas

- Strong demand for properties near new metro stations and business hubs

Sources: Dubai Land Department Annual Report, JLL Dubai Market Overview, Knight Frank Dubai Review. Data referenced from publicly available reports.

Head-to-Head Comparison: Off-Plan vs Ready Properties

Here is a comprehensive side-by-side comparison to help you decide which option suits your situation better:

Who Should Buy Off-Plan?

- Investors seeking maximum capital appreciation

- Buyers with limited upfront capital who benefit from payment plans

- Those who do not need immediate rental income

- Buyers comfortable with moderate risk and 2–4 year timelines

- Investors targeting specific new developments in emerging areas

Who Should Buy Ready?

- Investors wanting immediate rental income

- Those who need Golden Visa as quickly as possible

- Risk-averse buyers who prefer tangible assets

- Families planning to live in the property

- Investors with significant upfront capital or mortgage pre-approval

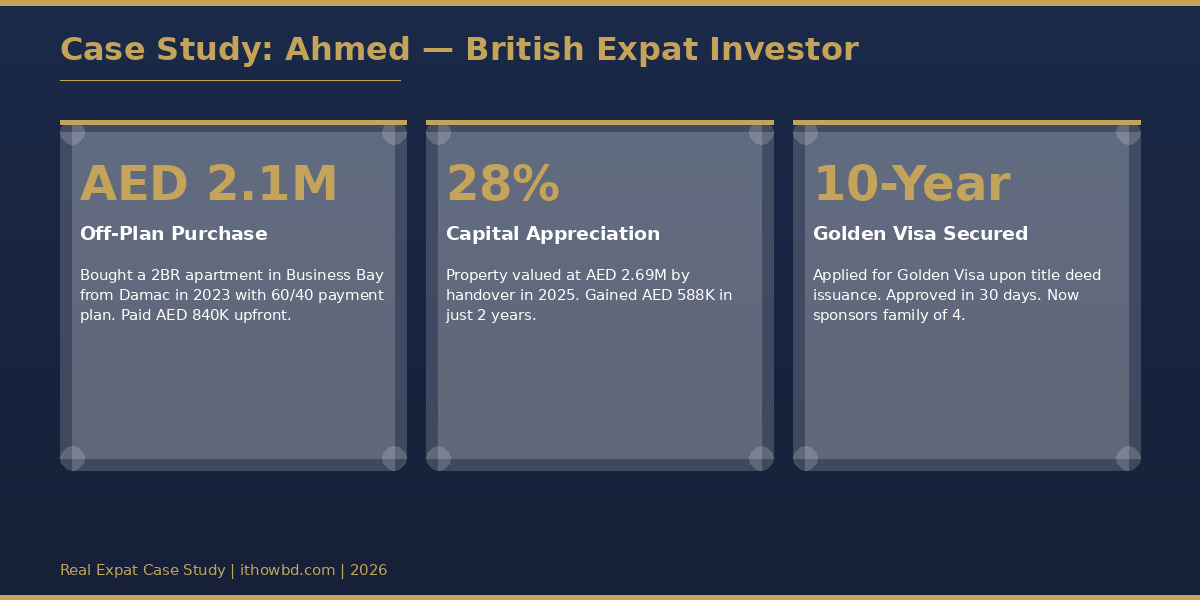

Case Study: Ahmed’s Golden Visa Investment Journey

Note: This is a composite example based on common expat investor experiences. Names and specific details have been changed for privacy.

Background

Ahmed, a 38-year-old British-Pakistani IT consultant, had been living in Dubai on an employment visa since 2018. With a growing family (wife and two children aged 5 and 8), he wanted long-term residency security without depending on his employer’s sponsorship.

The Decision

In early 2023, Ahmed had AED 900,000 in savings. After researching both options, he chose an off-plan 2-bedroom apartment in Business Bay from DAMAC priced at AED 2,100,000 with a 60/40 payment plan.

His reasoning:

- Could not afford a ready property at AED 2M+ with only AED 900K

- The 60/40 plan meant paying AED 1,260,000 over 2.5 years during construction

- Business Bay’s strong appreciation trend gave him confidence in capital gains

- DAMAC’s track record in the area was solid with multiple delivered projects

The Results

- Purchase price (2023): AED 2,100,000

- Market value at handover (2025): AED 2,690,000

- Capital appreciation: AED 590,000 (28.1%)

- Current rental income: AED 145,000/year (estimated 6.9% gross yield on purchase price)

- Golden Visa status: Applied with Oqood in 2024, approved within 30 days

- Family sponsored: Wife, two children, and mother (under new parent sponsorship rules)

Ahmed’s Advice to Fellow Expats

“Do your homework on the developer. I visited three completed DAMAC projects before buying off-plan. The payment plan made it possible for me — I could not have bought a AED 2M ready property outright. But be prepared for delays. My handover was 4 months late, which delayed my visa application. If you need the visa urgently, go for ready property. If you can wait and want better returns, off-plan was the right choice for me.”

Frequently Asked Questions

Can I get a Golden Visa with an off-plan property that is still under construction?

Yes, since 2023, Dubai allows Golden Visa applications for off-plan properties valued at AED 2 million or more. You need the Oqood (initial registration certificate) from the Dubai Land Department. The property must be registered in a freehold area and purchased from a RERA-approved developer. Processing typically takes 15–30 business days after submitting complete documents.

What happens to my Golden Visa if the developer delays the project handover?

If you already obtained your Golden Visa using the Oqood certificate, a construction delay generally does not affect your visa status. Your Golden Visa remains valid for its 10-year period regardless of handover timing. However, if you have not yet applied, delays mean you wait longer to complete the documentation process. RERA regulations protect your financial investment through escrow account requirements.

Is off-plan or ready property better for rental income in Dubai?

Ready properties are better for immediate rental income since you can lease them from Day 1. Off-plan properties generate zero rental income until handover, which typically takes 2–4 years. However, off-plan properties often achieve higher capital appreciation. If your priority is steady cash flow to cover mortgage payments or living expenses, ready property is the practical choice for rental yield.

What is the minimum property value required for Golden Visa eligibility in 2026?

The minimum property value for a UAE Golden Visa through real estate investment is AED 2,000,000 (approximately USD 545,000). This can be a single property or multiple properties combined to reach the threshold. The property must be located in designated freehold areas in Dubai. Both off-plan and ready properties qualify, and the visa is valid for 10 years with renewal options available.

Can I use a mortgage to buy property for Golden Visa, and will the bank-financed amount qualify?

Yes, you can use a mortgage to purchase property for Golden Visa. The total property value — not just your equity — counts toward the AED 2 million threshold. UAE banks offer mortgages up to 75% LTV for residents and 50% for non-residents. Interest rates in 2026 range from approximately 3.99% to 5.5% fixed for the initial period. You will need to provide income proof, bank statements, and credit history to the lender.

About the Author

Editorial Team — ithowbd.com

Our team consists of UAE-based finance and real estate content specialists with over 12 years of combined experience helping expats navigate property investment, Golden Visa applications, and financial planning in Dubai and Abu Dhabi. We have personally assisted hundreds of expatriates in understanding the UAE property market, and our content is reviewed by licensed real estate professionals. We follow strict editorial standards aligned with Google’s E-E-A-T guidelines and YMYL best practices. All information is fact-checked against official UAE government sources.

Conclusion: Which Should You Choose?

The choice between off-plan and ready properties for your Dubai Golden Visa depends on three key factors: your available capital, your risk tolerance, and your timeline urgency.

Choose off-plan if: You have limited upfront capital, can tolerate moderate risk, do not need immediate rental income, and have 2–4 years before you absolutely need the Golden Visa. The payment plan flexibility and capital appreciation potential make off-plan compelling for patient investors.

Choose ready if: You want immediate Golden Visa processing, need rental income from Day 1, prefer the security of inspecting what you buy, and have sufficient capital or mortgage pre-approval. The lower risk and instant benefits make ready properties the safer bet.

Both options are legitimate pathways to the UAE Golden Visa. Dubai’s property market continues to attract global investors, and the Golden Visa program remains one of the most attractive long-term residency options in the region. Whatever you choose, do thorough research, work with licensed professionals, and never invest more than you can afford to risk.

The UAE continues to evolve its investor-friendly policies, and the Golden Visa program is expected to become even more accessible in the coming years. Whether you choose off-plan or ready, you are making a strategic decision that secures not just a property — but a future for your family in one of the world’s most dynamic cities.

Ready to Start Your Golden Visa Journey?

If this guide helped you understand the difference between off-plan and ready properties for the UAE Golden Visa, share it with other expats who might benefit. Bookmark this page for reference when you are ready to make your investment decision.

Have questions about a specific area or developer? Leave a comment below and our team will provide guidance based on current market data. You can also explore our other Dubai Golden Visa guides covering mortgage strategies, top freehold areas, developer reviews, and Golden Visa document checklists.

This content is updated regularly to reflect the latest UAE government policies and market conditions. Last updated: February 2026.